The burden of credit card debt can be overwhelming, with the constant pressure of making minimum payments and the realization that interest charges are steadily eroding your hard-earned money. For many Americans, this is a daily reality, with the average household carrying over $8,000 in credit card debt. The promise of a single, lower-interest payment to replace multiple credit card bills can be tempting, but it’s essential to carefully weigh the pros and cons before committing to a personal loan. Understanding how a personal loan to pay off credit card debt works, its benefits, and potential alternatives can help you make an informed decision about your financial future.

Toc

- 1. Introduction to Personal Loan

- 2. When a Personal Loan to Pay off Credit Card Debt Might Be a Good Option

- 3. Factors to Consider Before Taking Out a Personal Loan

- 4. Related articles 01:

- 5. Navigating the Application Process

- 6. Alternatives to Personal Loans

- 7. Related articles 02:

- 8. Frequently Asked Questions

- 9. Conclusion

Introduction to Personal Loan

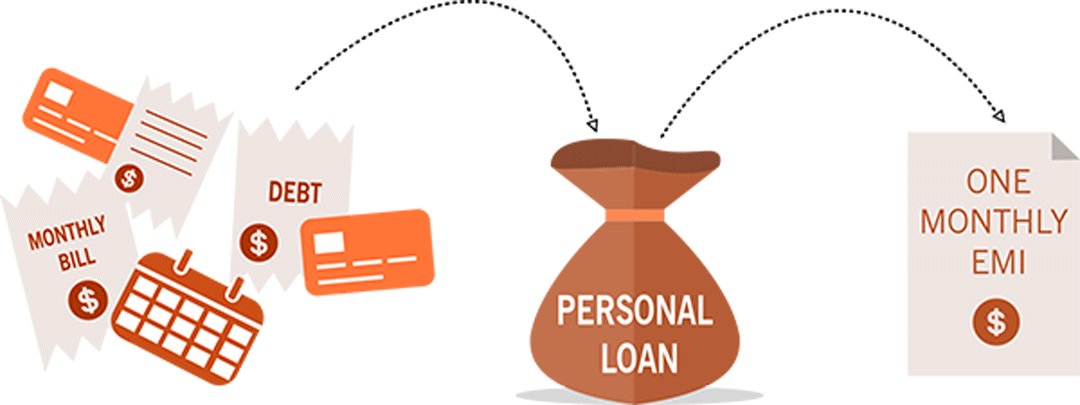

A personal loan is an unsecured loan that provides you with a lump sum of money, which you repay in fixed monthly installments over a set period, typically ranging from two to seven years. Unlike credit cards, personal loans have a fixed interest rate, meaning your monthly payment will remain the same throughout the life of the loan, making it easier to budget and plan your finances. Additionally, personal loans often come with lower interest rates compared to credit cards, particularly for individuals with good to excellent credit. This means more of your payment goes towards the principal balance rather than interest, allowing you to pay off your debt faster and potentially save money in the long run. However, it’s crucial to understand that a personal loan is not a one-size-fits-all solution, and it’s important to examine your unique financial situation before making a decision.

Pros of Using a Personal Loan to Pay Off Credit Card Debt

- Lower Interest Rates: As mentioned, personal loans often come with lower interest rates than credit cards, making them an attractive option for those carrying high-interest credit card debt. By consolidating multiple high-interest credit card balances into one lower-rate personal loan, you can potentially save hundreds or even thousands of dollars in interest payments over the life of the loan.

- Fixed Monthly Payments: With a fixed interest rate and set repayment term, personal loans provide predictability and stability when it comes to your monthly payments. This can make it easier to budget and plan your finances, as you know exactly how much you need to pay each month.

- Simplified Finances: Managing one personal loan payment each month is far simpler than juggling multiple credit card payments with varying due dates, minimum amounts, and interest rates. By consolidating your debt, you reduce the complexity of your financial obligations and minimize the risk of missing a payment, which can further impact your credit score.

- Potential Credit Score Improvement: Paying off credit card debt with a personal loan can have a positive effect on your credit score. This is because it reduces your credit utilization ratio, which is a significant factor in credit scoring models. By lowering your credit card balances and maintaining a lower overall credit utilization, you could see an improvement in your credit score over time.

Cons of Using a Personal Loan to Pay Off Credit Card Debt

- Potential Fees: Some lenders may charge origination fees, which can range from 1% to 8% of the loan amount. This fee can add to the overall cost of the loan and should be considered when evaluating the potential savings from a lower interest rate.

- Temptation to Accumulate New Debt: After paying off your credit card balances with a personal loan, it can be tempting to start using your credit cards again, leading to the accumulation of new debt. Without a disciplined approach to managing your spending, you may find yourself in a similar or worse financial situation down the line.

- Longer Repayment Terms: While personal loans can offer lower monthly payments, they may also come with longer repayment terms. This means you could be in debt for a more extended period, and even though the interest rate is lower, the total interest paid over the life of the loan may be higher than if you had aggressively paid down your credit card balances.

When a Personal Loan to Pay off Credit Card Debt Might Be a Good Option

Using a personal loan to pay off credit card debt can be advantageous under specific circumstances. Here are some key factors to consider:

The Appeal of Lower Interest Rates

According to recent data, the average interest rate for personal loans with a 24-month term was 12.35% as of December 2022, while the average credit card rate was 21.47%. For borrowers with excellent credit profiles, the lowest personal loan rates can be even more advantageous. For instance, a borrower with excellent credit might secure a personal loan with a 7% interest rate, significantly lower than the average credit card rate of 21.47%. This difference in interest rates can result in substantial savings over the loan term. If a borrower has a $10,000 credit card balance at 21.47% and consolidates it with a 7% personal loan, they could save over $1,000 in interest charges over a five-year period.

Simplifying Debt Management

Using a personal loan to pay off credit card debt can also simplify your financial life. Instead of juggling multiple payments with varying due dates and interest rates, a personal loan allows you to make a single monthly payment. This can reduce the stress associated with managing multiple creditors and help you stay organized.

Situations Where a Personal Loan Shines

There are specific scenarios where a personal loan might be particularly beneficial:

- High-Interest Credit Cards: If you have credit cards with interest rates above the national average, consolidating with a personal loan could save you money.

- Good Credit Score: If you have a solid credit score, you may qualify for favorable loan terms, making this option more appealing.

- Desire for Predictability: If you prefer a fixed repayment schedule, personal loans typically offer predictable monthly payments, which can aid in budgeting.

For example, a person with multiple credit cards carrying balances at interest rates exceeding 25% might benefit from consolidating their debt into a personal loan with a lower interest rate, even if their credit score isn’t exceptional. Similarly, individuals with a history of late payments or high credit utilization may find that a personal loan offers a more structured and predictable repayment path, helping them avoid late fees and further damage to their credit.

Factors to Consider Before Taking Out a Personal Loan

However, it’s crucial to carefully evaluate your specific situation before deciding on a personal loan. One key factor is your credit score and the interest rate you might qualify for on a personal loan. If your credit is on the lower end, typically below 670, you might be offered a personal loan interest rate that is still higher than your current credit card rates. In this scenario, consolidating your debt may not result in significant savings and could even lead to a higher overall debt burden.

Understanding Your Credit Score

Your credit score plays a significant role in determining the interest rate you’ll receive on a personal loan. Before applying, check your credit report for errors and take steps to improve your score if possible. This may include paying down existing debts, making timely payments, and ensuring that your credit utilization ratio is low.

3. https://alightmotion.top/discover-consolidation-loan-simplify-your-debt-save-money/

4. https://alightmotion.top/is-a-debt-consolidation-loan-a-good-idea-for-borrowers-with-bad-credit/

The Risk of Continued Debt Accumulation

Another important consideration is the risk of continuing to use your credit cards after consolidating your debt. While a personal loan can simplify your repayment process, it doesn’t address the underlying issue of overspending or poor financial habits. If you don’t address these root causes, you may find yourself right back where you started, accumulating even more high-interest credit card debt.

The Impact on Your Credit Score

Taking out a personal loan can affect your credit score in several ways. Initially, applying for a loan may result in a hard inquiry, which can temporarily lower your score. Additionally, closing credit card accounts after paying them off with a personal loan can negatively impact your credit score. Closing credit card accounts, especially those with a long history, can reduce your average credit age and increase your credit utilization ratio. It’s crucial to carefully consider the potential impact on your credit score before closing any credit card accounts. In some cases, it might be more beneficial to keep the accounts open, even with a zero balance, to maintain a good credit history.

If a personal loan doesn’t seem like the best fit for your situation, there are several alternative debt relief options worth exploring:

Debt Management Programs

Debt management programs, offered by nonprofit credit counseling agencies, can provide a structured approach to paying off your credit card debt. These programs typically involve negotiating lower interest rates with your creditors and a consolidated monthly payment plan. According to industry data, over 80% of individuals who enroll in a debt management program successfully complete it, with the majority reporting that they were able to pay off their debt faster than they would have on their own.

How Debt Management Works

The process usually starts with a consultation where a credit counselor reviews your financial situation. They will help create a personalized debt management plan tailored to your needs. Instead of making multiple payments to different credit card companies, you’ll make a single, consolidated payment to the credit counseling agency, which will then distribute the funds to your creditors.

Debt Consolidation Programs

Debt consolidation programs, similar to personal loans, allow you to combine multiple credit card balances into a single, lower-interest payment. However, these programs are typically offered by specialized lenders or financial institutions, often with more lenient credit requirements compared to traditional personal loans.

Credit Counseling Services

Seeking guidance from a certified credit counselor can be invaluable when navigating the complexities of credit card debt. These professionals can review your financial situation, provide personalized advice, and help you explore the most suitable debt relief options for your needs.

Debt Forgiveness Programs

As a last resort, debt forgiveness programs may be an option. These programs involve negotiating with creditors to settle your debts for less than what you owe. While this can provide significant relief, it’s important to understand the potential risks, such as the impact on your credit score and possible tax implications on forgiven debt.

Alternatives to Personal Loans

Before deciding on a personal loan, it’s important to consider other options that may be available to you:

Balance Transfer Credit Cards

Balance transfer credit cards can be an effective way to manage existing high-interest credit card debt. These cards offer a promotional period, typically ranging from 6 to 18 months, with 0% interest on transferred balances. During this period, your payments go directly toward reducing the principal balance, potentially allowing for faster debt reduction. However, it’s essential to consider the balance transfer fee, usually between 3% to 5% of the transferred amount, which can add to your total cost. Additionally, be aware of the terms and conditions: the interest rate will revert to a higher standard rate once the promotional period ends, so it’s crucial to pay off as much of the debt as possible within that time frame.

Home Equity Loans

Home equity loans, also known as second mortgages, allow homeowners to borrow against the equity in their property. These loans often come with lower interest rates compared to personal loans and credit cards, making them an attractive option for debt consolidation. However, it’s important to recognize the risks involved; your home serves as collateral, meaning that failure to repay the loan could result in foreclosure. Before considering a home equity loan, carefully assess your ability to make consistent payments.

1. https://alightmotion.top/discover-consolidation-loan-simplify-your-debt-save-money/

2. https://alightmotion.top/is-a-debt-consolidation-loan-a-good-idea-for-borrowers-with-bad-credit/

Peer-to-Peer Lending

Peer-to-peer (P2P) lending platforms connect borrowers directly with individual investors willing to fund loans. These platforms can offer competitive interest rates and more flexible lending criteria than traditional banks. For individuals with unique financial situations or lower credit scores, P2P lending might provide a viable alternative to conventional personal loans. Nonetheless, it’s important to research and understand the platform’s fees, terms, and the responsibilities associated with this type of borrowing.

Using a Savings Account or Emergency Fund

If available, tapping into your savings or emergency fund can be a prudent option to manage debt. Utilizing your own resources prevents accumulating additional debt and interest costs. However, depleting your savings should be a carefully weighed decision, especially if it leaves you without a financial safety net for unforeseen expenses.

Borrowing from Family or Friends

Another alternative might be borrowing money from trusted family members or friends. This can often come with little to no interest and flexible repayment terms. It’s imperative to approach this option transparently and responsibly to avoid potential strains on relationships. Drafting a formal agreement detailing the loan terms can help maintain clarity and trust for both parties involved.

Frequently Asked Questions

Q: How do I know if a personal loan is right for me?

A: Before considering a personal loan to pay off credit card debt, evaluate your credit score, current interest rates, and your ability to manage your spending. If you can qualify for a personal loan with a significantly lower interest rate than your credit cards, and you’re confident you can avoid further debt accumulation, a personal loan may be a viable option.

Q: What are the risks of taking out a personal loan to pay off credit card debt?

A: The primary risks include the potential for a higher interest rate if your credit is not stellar, the possibility of continuing to use credit cards and accumulating more debt, and the impact on your credit score from closing credit card accounts.

Q: What are some alternatives to a personal loan for credit card debt?

A: Alternatives include debt management programs, debt consolidation programs, and working with a credit counseling service. These options may offer more structured repayment plans, lower interest rates, and assistance in addressing the underlying causes of your debt.

Q: How do I find a reputable lender for a personal loan?

A: To find a trustworthy lender, compare offers from multiple lenders, check online reviews, and consider working with a credit union or community bank, which may offer better terms and personalized service.

Conclusion

When it comes to managing and paying off credit card debt, using a personal loan can be a useful tool, but it’s not the only solution. By carefully considering your credit profile, spending habits, and alternative debt relief options, you can find the best path forward to achieve financial stability and become debt-free. Remember, seeking guidance from qualified financial professionals can be invaluable in navigating the complexities of credit card debt and exploring the most suitable strategies for your unique situation. Whether you choose a personal loan to pay off credit card debt or explore other options, taking proactive steps today can lead to a more secure financial future.